We were rather optimistic - ESI, April 2026

The economic pessimism enters ints 10th month and consumer confidence reaches the second lowest value amongst EU nations.

Romania never excelled economically. If a growth in private consumption with one of the lowest innovation scores in Europe is called business excellence, then I take my words back.

We were up there, but now it is all going down.

Romania pivoted in the late 2010s to an alternative growth model. Exports were still attractive (less tho), given our self-branded status of a “cheap labor costs” country though production was shifting Eastwards. Exports were not imagined to be the growth mechanism, so the economic architects pushed the pedal hard for wage-led growth.

Raise wages, lower taxes, boost consumption and keep on repeating the same cycle over and over again. Deficit was lower back then, the country was not facing an excessive deficit procedure and the solution looked alright on paper. Towns developed, people’s wages went up and the economy seemed solid.

Until now.

That growth model faced a major wall in Romania: imports. We consumed more, but also imported way more. Importing more goods and services pushed our current account balance to such a high level (around 8,0% GDP in 2025) which, in turn, exercised pressures on our currency. Add the deficit, the political crisis, the war in Iran and all of a sudden Romania is trying to traverse a paradigm shift while still preserving some optimism for the economy.

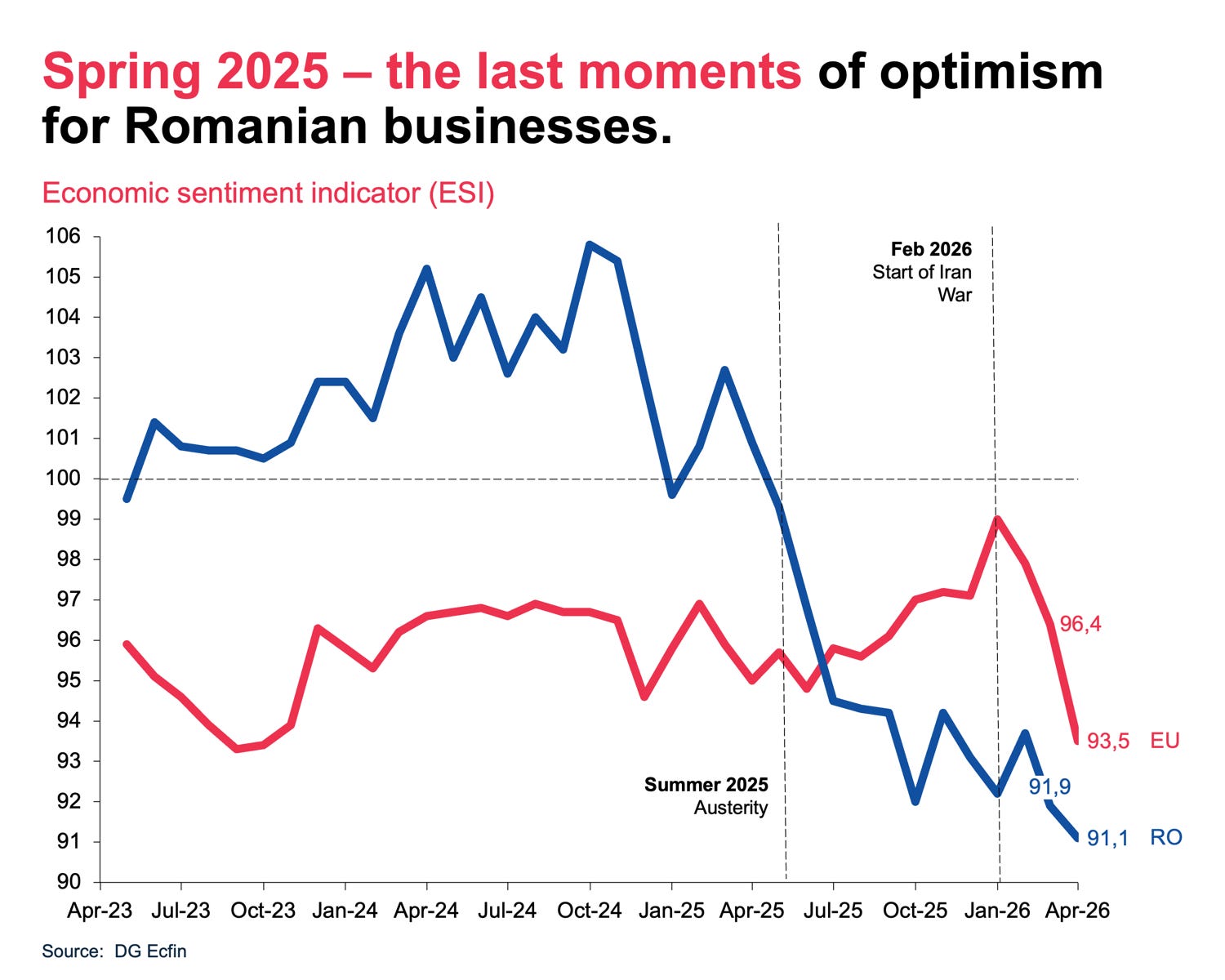

Economic sentiment indicator - April 2026

In April 2026, the Economic sentiment indicator (ESI) reached 91,1 in Romania, down 0,8pp from 91,9 the month before. For the 10th consecutive month, Romania’s ESI is lower than the EU average.

The contraction in April 2026 corresponds to a worsening sentiment regarding the War in Iran. The EU average ESI went down 2,9pp from 96,4 in March to 93,5 in April 2026.

Between February - April 2026 almost all European countries1 faced major contractions in their ESI. The EU average contraction was 5,5pp, reaching values as high as 14,3pp in Malta. Romania scored one of the lowest contractions during February - March 2026, just 1,1pp, because it already faced a low ESI amid a severe downgrade in the summer of 2025.

If we were to imagine the country with no political crisis, no annulment of elections, no high twin deficits (you get the point), perhaps Romania would have been up there, just like before. Mid-2025 Romania went into negative territory (ESI getting below 100), representing a major paradigm shift for a country that managed to stay above the 100 mark for years.

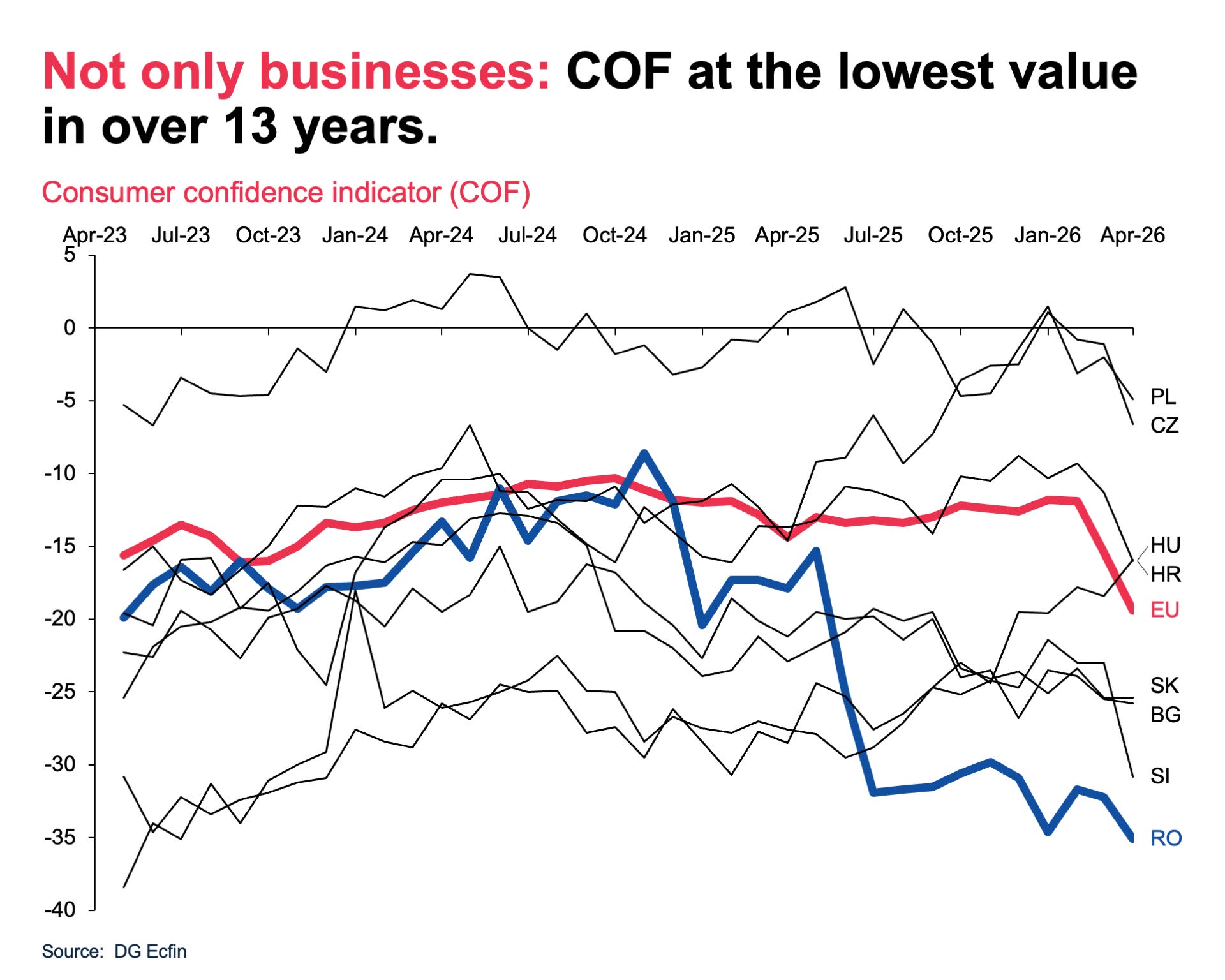

The low ESI score corresponds to a low consumer confidence indicator (COF) as well. Leaving aside Greece (COF: 54,7), Romania scored the lowest (-35,1) amongst all the other EU nations. Again, just like the economic sentiment indicator, we were never last and our feelings towards the economy seemed slightly better before.

That was the past because the summer of 2025 marked a major contraction in the COF indicator, practically decoupling Romania from the EU average. Sure, the War in Iran brought the indicator further down, but the shock was smaller in size for Romania. Why? The consumers already priced a worse economic outlook months before after last year’s debacle. In May 2025, Romania’s COF was at 15,3, then it went down to 25,1 in June, 31,9 in July and settled around 31,7 in August 2025. Practically, it more than doubled during those three months.

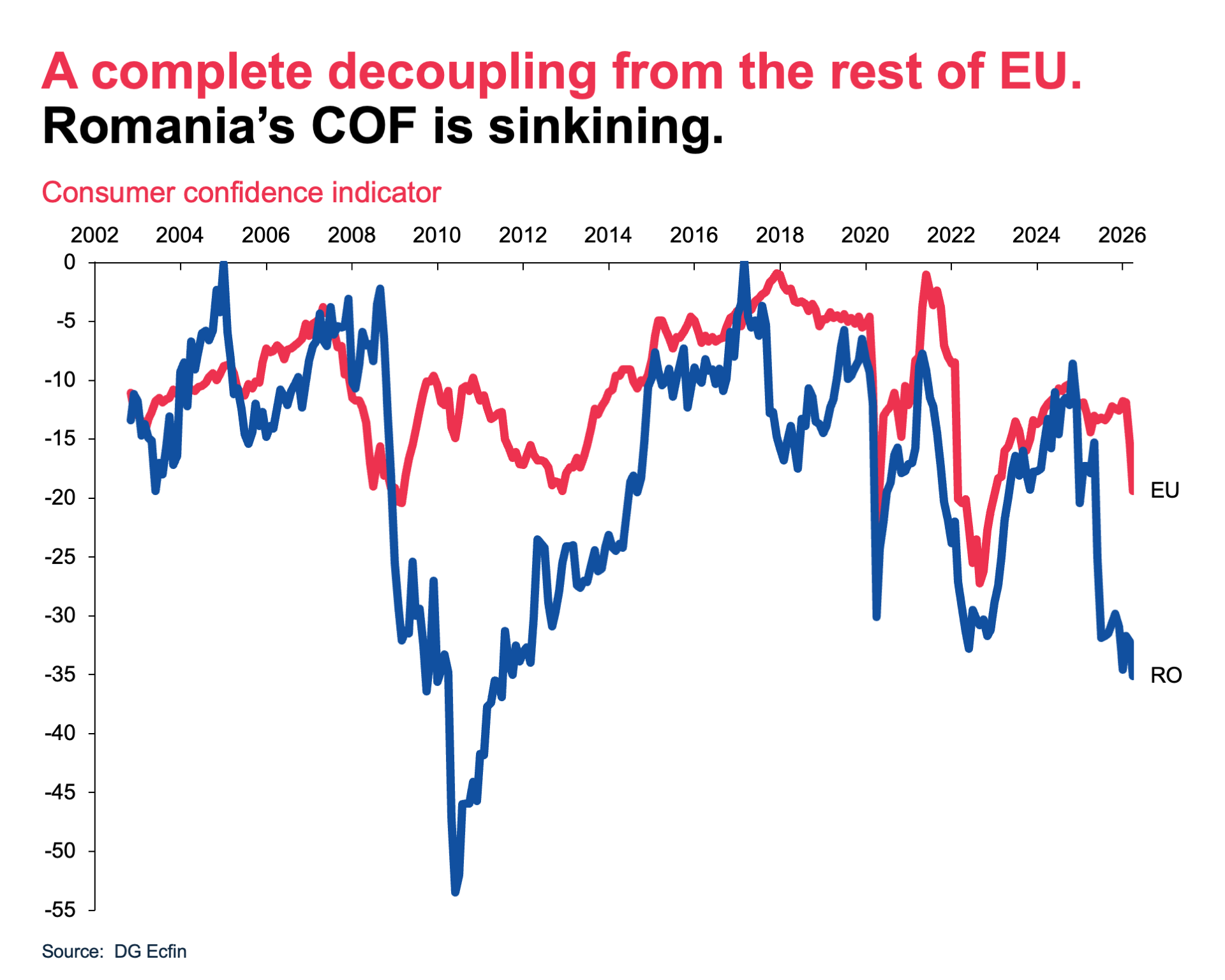

Previously, the EU and RO consumer confidence indicator used to go hand in hand since 2015. Slight differences occurred between 2018 and 2020, though for the most part the difference between the two was rather small.

The Great Financial Crisis pushed the COF indicator to such a low level in Romania from which it only recovered years later in 2025. Sure, the EU COF also went down, but the magnitude was nothing compared to what Romania went through.

Now the moment looks slightly similar, another decoupling, sinking once again lower and lower. It all depends on how long the war keeps on going and how impactful supply bottlenecks will be on inflation in the long term. If the war ends tomorrow and everything reopens, Romania should not expect a high jump to a 2024 confidence level, but rather a slow uptick, putting us back in the same pessimistic spot we were in back in February.

More importantly, the growth model focused on consumption will no longer be the dominant force unless the country wants to experience an even higher pressure on its currency. Most probably not, so investments it is.

Given that the government will continue its attempts at putting consumption in its own place, there should be no significant rebound in the consumer confidence indicator anytime soon. Unless consumers whose purchasing power has been going down witness a major economic expansion, the following years will represent a prolonged pessimistic feeling.

Wrapping it up… GDP, ESI.

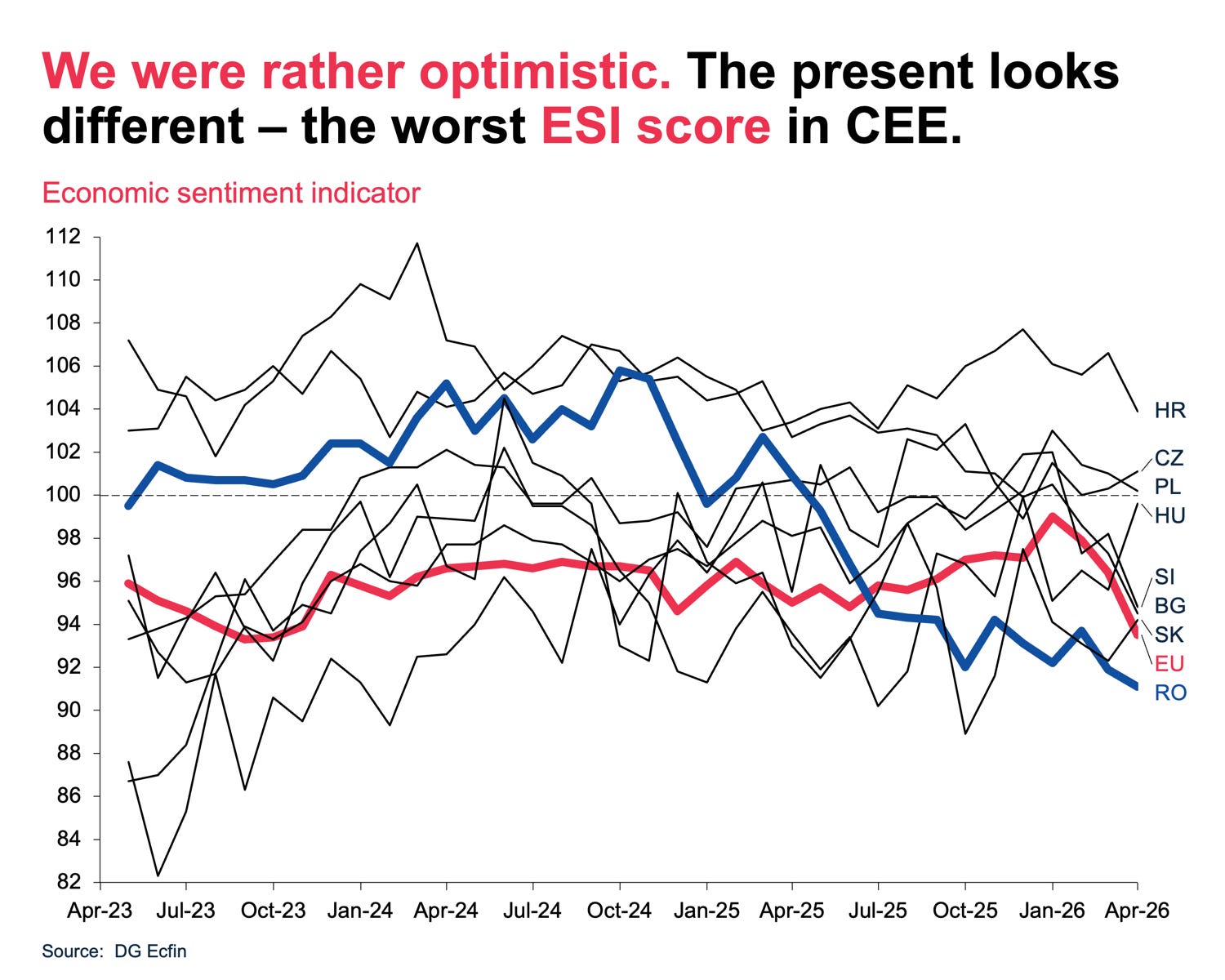

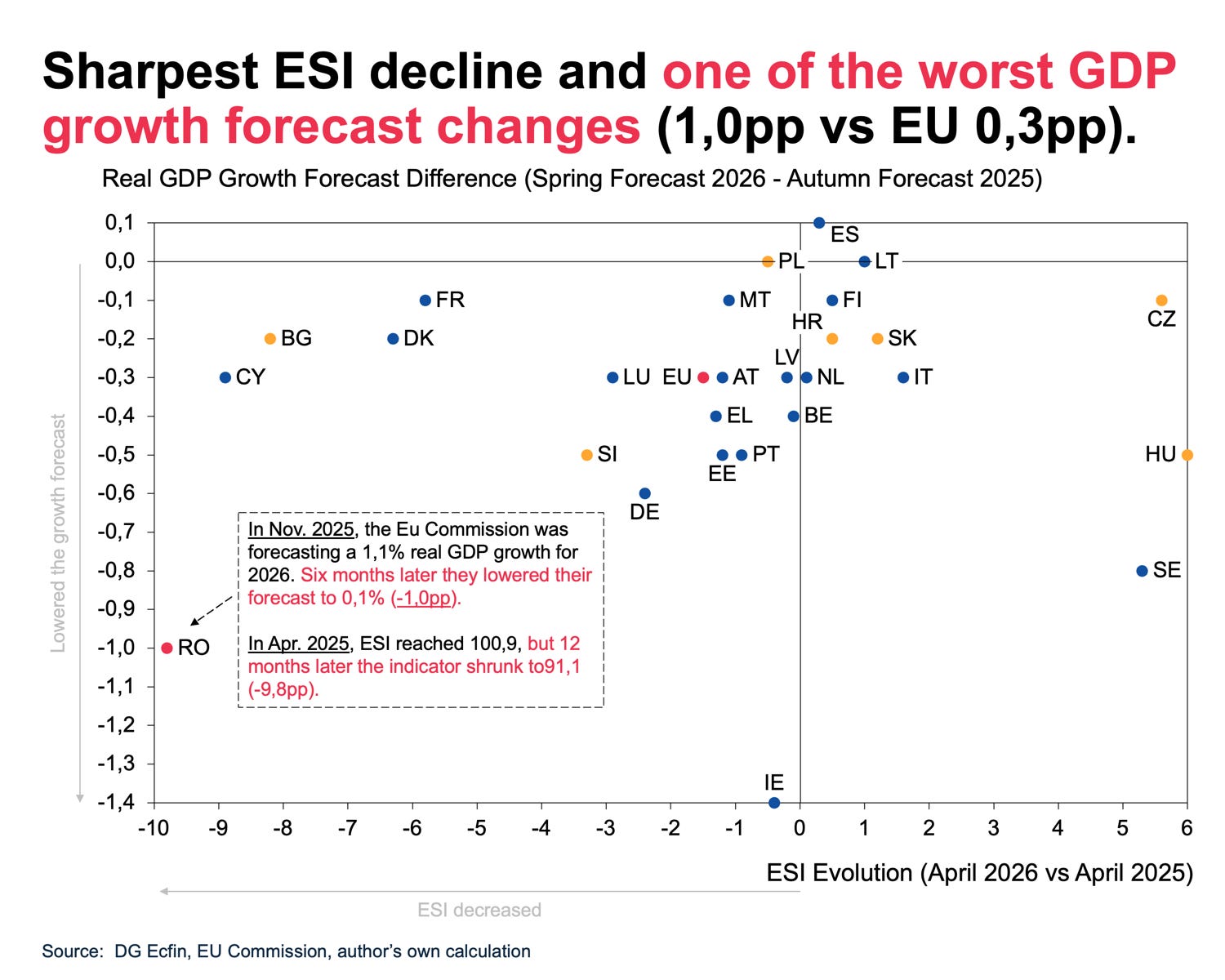

But let us move our focus from the COF once again to ESI. If we were to plot on a scatter graph the real GDP growth forecast difference between November 2025 and May 2026 and then the ESI y/y evolution, we would witness a lonely Romania, isolated in its own corner.

If we leave aside Ireland, Romania is facing the highest 2026 GDP growth forecast correction (-1,0pp), moving down from 1,1% to 0,1%. That -1,0pp correction corresponds to a decrease of 9,8pp in ESI - the largest amongst EU countries.

Keeping those in mind, one is bound to ask: where will this end? Chances are we will hit a brick wall, though it all depends on how long the war lasts and what inflation will look like. There was a rebounding chance, though I believe we have missed that train since we no longer have a functional government.

Investments will be the way the economy will grow years from now, though the country is facing major issues getting the National Resilience and Recovery Plan to its final stop. It is not a problem of having lost momentum in a marathon, but rather we have not even entered the races we signed up for.

See you soon. What do you think about those short notes? Would you like to see more of them?

Except Hungary (+4,5pp), Luxembourg (+4,4pp), Greece (+0,6pp) and Slovakia (+0,1pp).